Into a portfolio squeeze, eye’s wide shut?

Liquidity risk to investors balance sheet is on the rise.

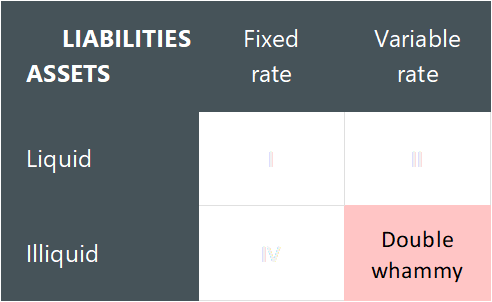

Should inflation stay sticky and Central banks accelerate monetary withdrawal – will investors then find themselves in a double whammy, caught between skyrocketing financing cost and locked up in illiquid investments, again?

This situation is not eminent. However, the setup is there with all the traditional hallmarks. In case this eventually materialise, investors will be forced to sell what they can, and not what they should.

A short review of characteristics of such a scenario, and importantly how they may be avoided. Spoiler alert; it’s easy – avoid stepping into one.

Falling interest rates

Before examining a tricky reaction to rising interest rates, recall the effect on asset prices of interest rates sliding for the past 40 years.

Falling interest rates have been a/the? principal explanation why assets prices have gone up – stocks, bonds, real estate. Everything with a cash-flow has been inflated by a basic asset pricing accounting technical. The high tide has lifted all boats.

Where to look

Today, yield starved investors are heavily loaded on their asset side in illiquid investments. Typically; private equity, private debt, real estate and similar. We estimate that allocations to illiquid investments are at an all-time-high and with institutional investment managers only looking to increase that share further.

Product providers have been more than happy to meet the demand, as these products have the added benefit of locking-up client assets with them, typically for periods of 10-15 years. Not a life sentence, but still.

Now, the liquidity risk we will here address, is defined by how easily an asset can by traded in a transparent and efficient marketplace without any significant impact to the market price in any direction.

Investors in Apple Inc will for any big or small market move see the impact on their portfolio in real-time as this asset is marked-to-marked.

Investors pay less attention to their illiquid investments as the price move is slow. This is deceptive as in a fast-rising interest rates scenario, most of such assets are negatively affected. The majority even more so, as they typically have the characteristic of razor thin margins and high leverage.

The pricing of such assets is performed by off-market accountants and actuaries with a frequencies of say, a quarter or a year. There’s a risk that such calculations for Internal Rates of Return is still based on the assumption interest rates will remain near zero, as was the case, only a few weeks ago.

We believe now is a prudent time to investors to revisit the composition of their overall balance sheet, particularly in respect to overall liquidity and interest rate sensitivity.

For the opportunistic investors in liquid assets this would simultaneously provide for an opportunity. A “fire sale” would somewhat paradoxically first hit liquid assets. This would provide for the one occasion we know of for the possibility of buying real “value”.

And finally, should illiquid assets suddenly be revalued towards degrees of toxicity, some may wonder who end up being the patsy. Sell, if history is any guide, the answer is your pension fund (9 minutes watch, but worth it).

Reading Time: 3 minutes