Active Risk Allocation (ARA) update:

The recommended portfolio risk allocation is slowly falling below neutral after an extended period of elevated risk exposure. Several factors are changing yet again and none of the changes are for the better. USA’s failure in handling the CoVid-19 pandemic is now beginning to impact global growth, slowing the recovery.

Factor group |

Tendency |

| Fundamentals | Weakening |

|

The initial post-covid-19 recovery is already fading Stock market expectations are still that a strong economic recovery will happen in Q3. USA’s CoVid19 fight is out of control and is likely to delay any recovery. US weight in global economy will impact global recovery. Many support packages were predicated on a full reopening by 1 July. More help to come but less significant than in March |

|

| Risk & Volatility | Increasing |

|

Coordinated monetary and fiscal expansion have lifted all asset prices. It means that correlation between asset classes have increased and diversification gains have diminished. Markets are more vulnerable, as last seen in February. |

|

| Market Intelligence | Factors underpinning upbeat stock markets are fading |

|

Stock markets have tried to “look through” to the end of the pandemic. This is now slowly changing to a focus on potentially longterm effects of the pandemic. Economic surprises are now heading south and will be in negative territory early August. On current trends market sentiment could take a hit later in August. Real interest rates are low and unlikely to fall significantly lower. No further support to risk assets from here. |

|

| Technicals | Divergence in otherwise stable trends |

|

Trends in stock and bond markets simultaneously point upwards. Stock markets may end up stretched. Increasing risk that the stock markets end up disappointed while prices in overbought territory. |

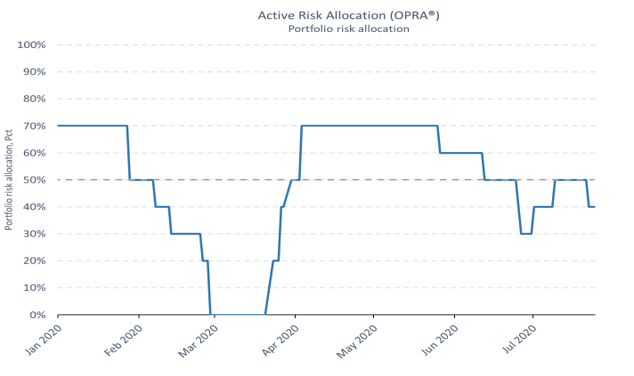

Proprietary indicators

Our Portfolio Risk Allocation indicator has had a dramatic run this year, from a 70% count in January and in April-May.

In February as well as in June, the fall in the indicator is mainly a reflection of the increased correlation in the main asset classes and the corresponding lack of diversification (except for cash). Add that stock market sentiment is weakening and macroeconomic fundamentals fading.

Macroeconomics do not develop quickly. Given the fading speed of the recovery and the likely tapering off of the economic stimulus packages we would be surprised if the downtrend indicator were to revert any time in the near future.

________________________________________________________________________________________________________________________

For more details about our asset allocation method, consult our Asset Allocation page

Reading Time: 2 minutes